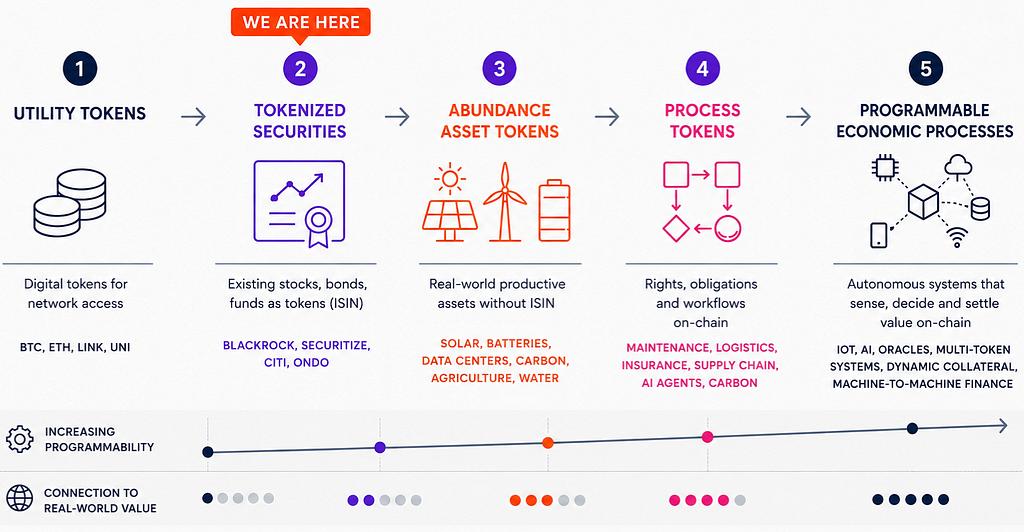

We are at stage 2 of 5

Jul 11, 2026 · Silver

Jul 11, 2026 · SilverWhere tokenization actually is, what the next three stages look like, and why the road takes ten years.

I made this map to sort out my own thinking. Five stages, from utility tokens to autonomous economic systems. The most important part is the orange tag. We are at stage 2.

That is worth saying plainly, because every conference panel this year has announced the arrival of the programmable economy. The map disagrees. What has arrived is stage 2: existing securities, wrapped as tokens.

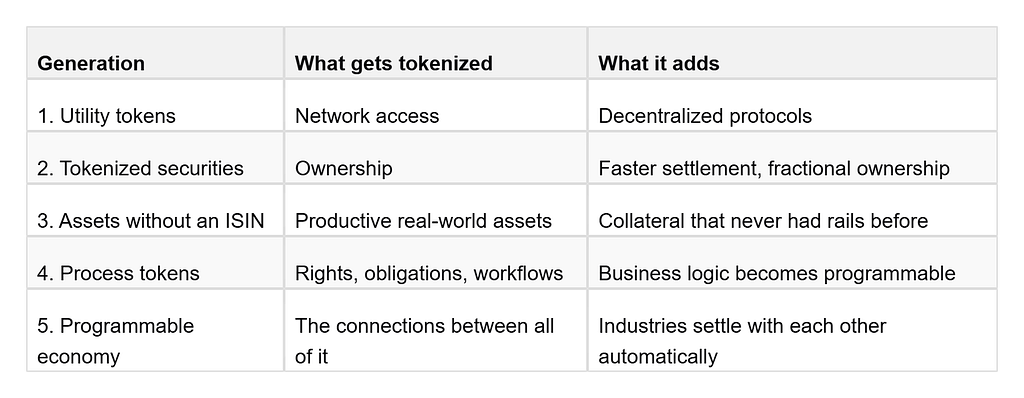

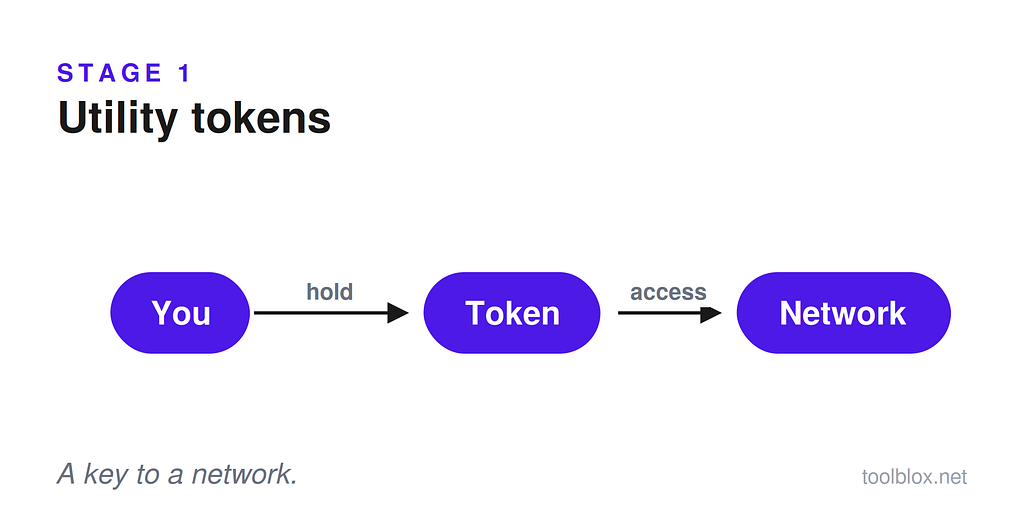

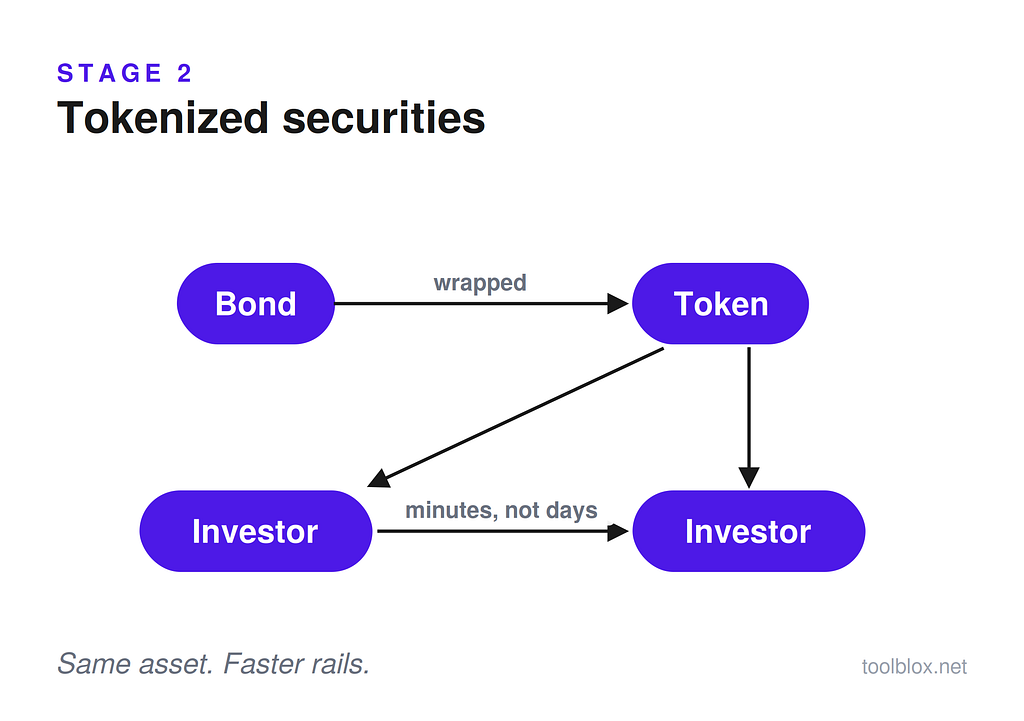

Each stage tokenizes a different thing:

Stage 2 is real. It is also a plumbing upgrade.

Stage 2 works. BlackRock runs a tokenized fund. Securitize, Ondo and a dozen others are moving stocks, bonds and money market funds onto chains. Settlement gets faster. Administration gets cheaper. Aave launched Horizon, a permissioned market where institutions borrow stablecoins against tokenized treasuries. This is genuine progress.

But notice what stage 2 assets have in common: they already had rails. A bond has an ISIN, a transfer agent, an exchange, a custodian. For these assets, tokenization is an efficiency upgrade on infrastructure that already exists. Useful, crowded, and commoditizing fast.

It also explains a puzzle. Tokenized real-world assets on public chains total roughly $30 billion as of mid-2026, per rwa.xyz, and that is after tripling in a year. Nearly every large bank has a digital assets team working on this, and the result is still a rounding error against the hundreds of trillions in global assets. When the pitch is “same asset, cheaper plumbing,” adoption becomes a cost-benefit spreadsheet. Spreadsheets move slowly.

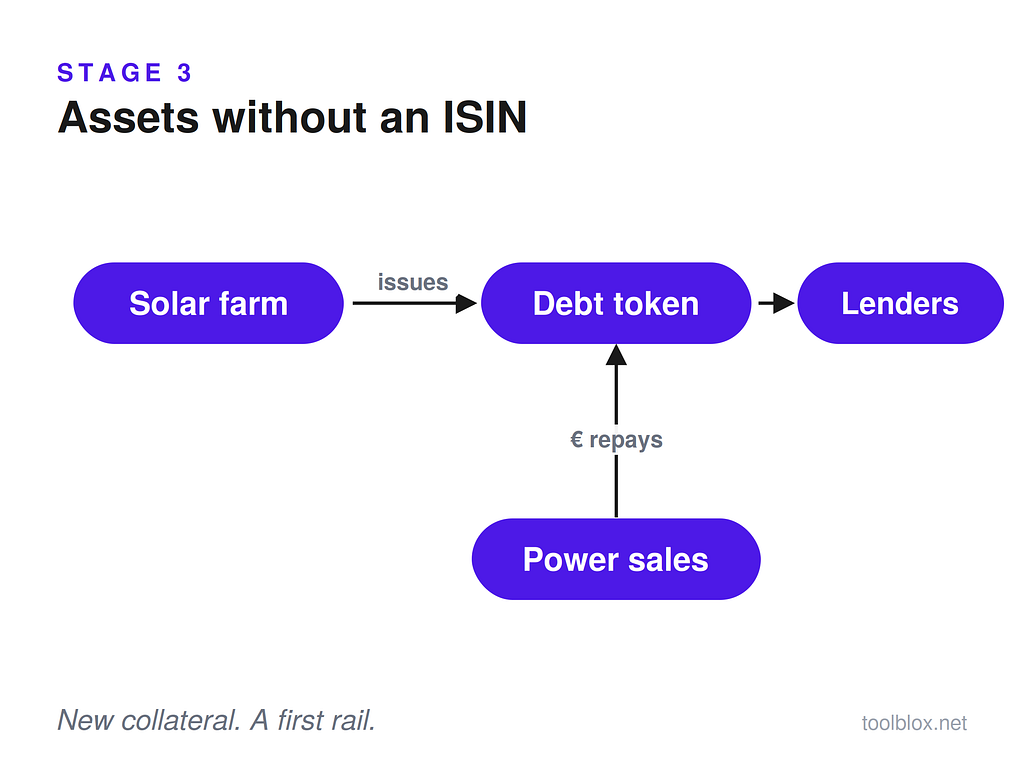

Stage 3: assets without an ISIN

The next stage is different in kind, not in degree. It tokenizes assets that never had financial infrastructure at all. Solar project debt. Battery storage revenue. Invoice pools. Royalty streams. Machine fleets.

These assets have no transfer agent to disrupt and no exchange listing to speed up. For them, tokenization is not an efficiency gain. It is the first financial rail they will ever get.

Aave’s founder Stani Kulechov calls these abundance assets, and makes the case with solar: predictable cash flows backed by twenty-year power purchase agreements, modular projects, hungry capital on one side and a financing bottleneck on the other. But solar is one aisle in a very large store. The Asian Development Bank measures a global trade finance gap of $2.5 trillion a year: real orders from real businesses that banks decline to finance, with 41 percent of SME requests rejected. Private credit is a roughly $3 trillion market where loans trade by phone call, if they trade at all. Different industries, same structure: productive assets want liquidity, capital wants productive collateral, and very little connects them.

So take one solar farm and put its debt on chain as a token. Lenders hold the token. Revenue from the power contract pays it down. That is stage 3: one asset, one token, real cash flow. Now keep going.

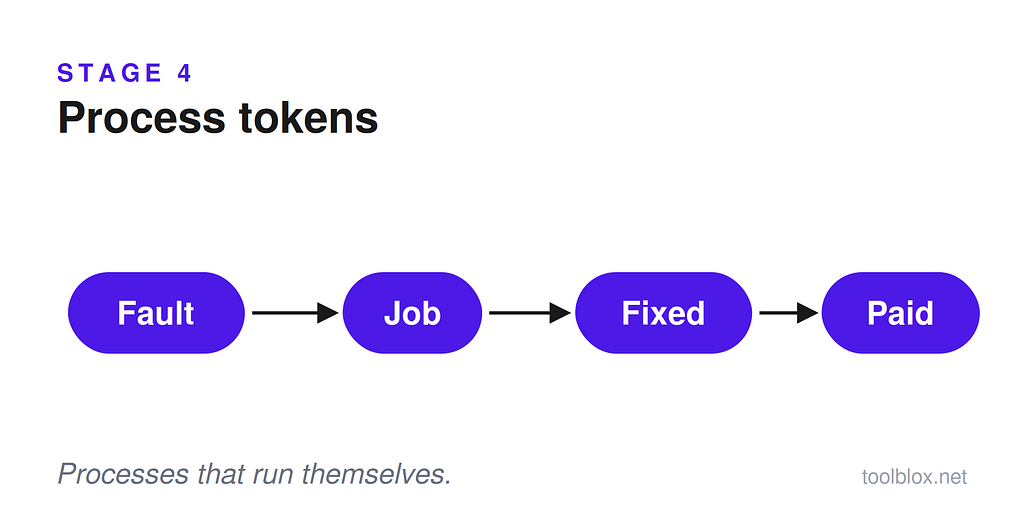

Stage 4: the same farm, but the processes

Stage 4 tokenizes the farm’s processes, not just its debt.

Maintenance becomes a workflow: the inverter reports a fault, a work order opens, a contractor accepts, the meter confirms output is back, payment releases. Insurance becomes a workflow: the weather feed reports hail, the claim pays, no adjuster visits the site.

Each process is a few states, a few rules and a payout. Each one is boring on its own. That is the point. Boring processes are the ones you can trust to run without you.

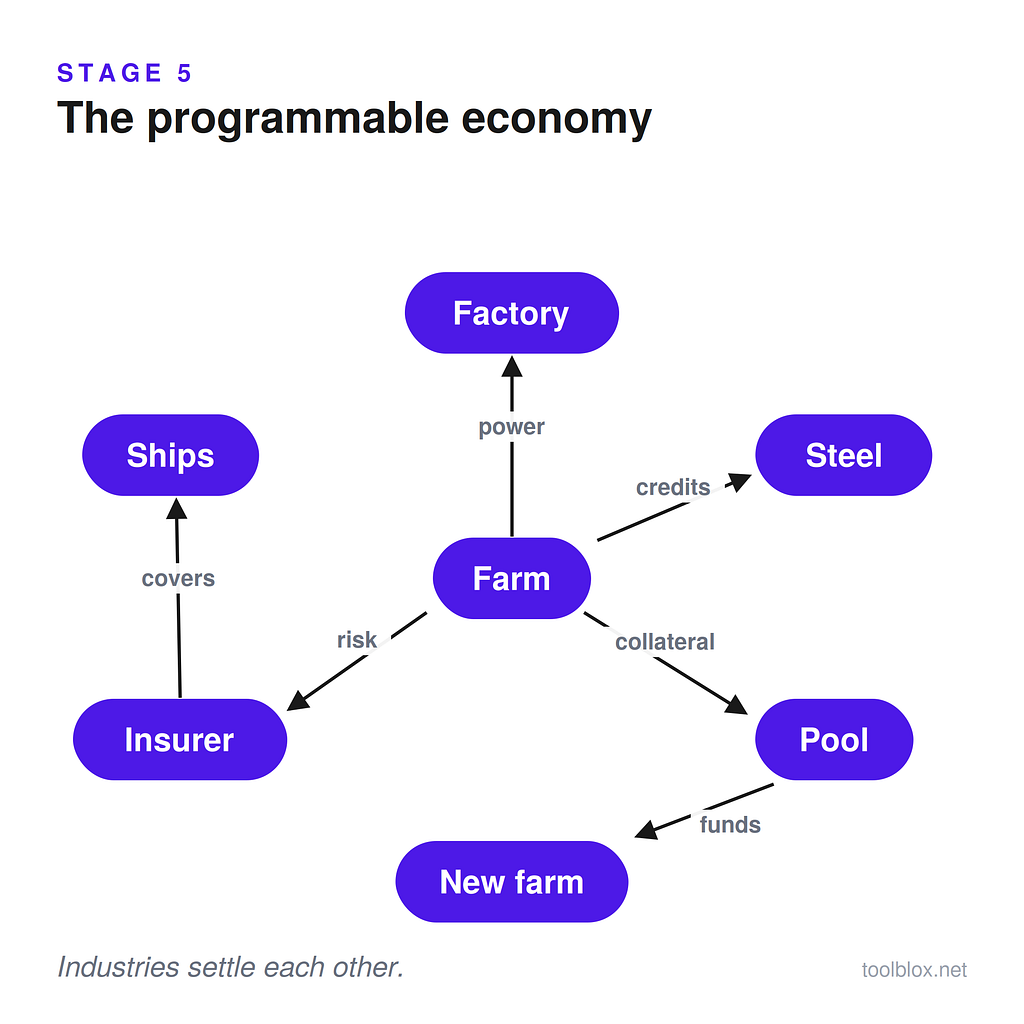

Stage 5: the workflows leave the farm

So far, everything happened inside one company. Stage 5 is what happens when workflows from different industries start reading each other. Follow the same farm through one sunny afternoon.

The meter counts output. The power contract bills the factory next door. The factory has a contract of its own: when solar is cheap it runs its furnaces, and when clouds come it earns money by pausing them. Energy and manufacturing just settled with each other. Nobody called anybody.

The clean output is confirmed and carbon credits mint. A steel plant two countries away buys them automatically, because its own compliance workflow noticed it was getting close to its emissions cap. That is a third industry in the chain.

Revenue lands at the farm. The debt token takes its share first, by rule. And that debt token is not sitting in a drawer. It is collateral in a lending pool, and the pool’s depositors are funding construction of the next farm. Finance is now in the chain, running itself.

The farm’s hail insurance passes a slice of its risk to a reinsurance pool. The same pool covers container ships. When a storm hits either one, payouts move by trigger and next season’s premiums adjust on both sides.

Count what happened. Energy, manufacturing, carbon, credit and insurance settled with each other in one afternoon. Nobody sent an invoice, called a broker, or approved a payment. Every decision was made earlier, when someone drew the rules.

One thing makes this hard, and it is not the technology. Every arrow in that chain moves money between parties who do not trust each other. The lender, the operator, the power buyer, the insurer, the steel plant. The rules cannot live in any one party’s database, because everyone else would have to take their word for it. The rules have to be enforced by the contract itself. That is the entire reason any of this belongs on a chain.

Why this is inevitable

Every large buildout in history needed a new financing instrument before it could scale. Railways got the corporate bond. American homeownership got the thirty-year mortgage, and ownership went from 44 percent in 1940 to nearly 70. The instrument is never a nice-to-have. It is the thing that turns a technology into an economy. Assets without an ISIN are waiting for theirs.

The first-order benefit is the cost of capital. Buyers of assets they cannot resell demand a discount, and finance has measured it for decades: in restricted-stock and private-market studies, the illiquidity discount runs 20 to 30 percent. Run that machine in reverse. Make the asset tradable and the discount shrinks, which means the issuer can promise a lower return and still find buyers. On infrastructure and private credit measured in trillions, a few percentage points of capital cost is the whole game. Liquidity also changes how much money is allowed to show up at all. Institutions cap what they may hold in assets they cannot exit, so the same project attracts a multiple of the capital in liquid form.

The banks have run their own numbers on the market. McKinsey’s conservative estimate is about 2 trillion dollars of tokenized assets by 2030. Citi projects 4 to 5 trillion. BCG’s estimate is 16 trillion. Today’s market is a few tens of billions. Take the most pessimistic bank on that list and the market still grows close to a hundredfold this decade.

The second-order benefit is recycling. Liquid assets move. An investor buys tokenized solar debt, holds it three years, sells, and funds the next project with the same money, so one dollar finances several projects over a decade instead of sitting locked in one. This is already running at small scale: on-chain private credit holds several billion dollars in live loans, per rwa.xyz, funded on-chain and tradable from day one. And markets appear where none existed. Farm debt, royalty streams and machine fleets get a price for the first time.

The third-order benefit is the boring trillion: administration. When the meter is the invoice, billing, collections, reconciliation and claims adjustment become code. Both sides of every transaction read one shared state, so disputes shrink to the cases where reality is genuinely unclear. Finance gets the cost curve it never had. Like solar panels, the cost per transaction falls as volume grows, instead of staying flat forever.

The fourth-order benefit is what becomes possible. Close even part of that $2.5 trillion trade finance gap and the growth lands exactly where banks reject 41 percent of applications today: small exporters. The money leg has already proven itself at scale. Stablecoins settled a headline $33 trillion in 2025, against Visa’s roughly $17 trillion fiscal year, and even the strictest bot-filtered estimates put organic volume near $10 trillion. And there is a new customer that cannot use the old system at any price: software. AI agents cannot open bank accounts, cannot sign paper mandates, and cannot wait three days for a wire. Machine commerce does not prefer these rails. It requires them.

None of this needs believers. The moment one solar operator refinances at the liquid rate, every competitor is four points of capital cost behind, and follows or loses. Adoption will happen the same way stage 2 was slowed: by spreadsheet. The spreadsheet moves slowly. It also never moves backward.

Why this takes ten years

I have made stage 5 sound close. It is not. I think it is eight to ten years away for the leading industries, longer for the rest. It is worth being honest about why, stage by stage.

Stage 3’s obstacle is the buyers. The people who own productive real-world assets are the most conservative buyers in finance. A solar operator’s entire business is refusing risk on the money side: bank debt, twenty-year power contracts, insurance on everything. They are paid to be late to new things, and they are good at their jobs. They will not adopt tokenized debt because a whitepaper is elegant. They adopt when their bank recognizes the token as collateral, when their lawyer confirms it holds up in their jurisdiction, and when someone else in their asset class went first and survived a dispute. So stage 3’s prerequisites are mostly legal, not technical: securities wrappers that courts accept, banks that can hold the asset, and one brave first deal per asset class. There is also a data prerequisite. A token backed by a power meter is worth exactly as much as the meter’s honesty.

Stage 4’s obstacles are rails, data, and control. Three prerequisites here. First, cheap and fast chains. A maintenance workflow fires hundreds of small state changes, and in 2021 each one cost dollars and took minutes. On today’s L2 networks it costs cents or less and settles in seconds. This one is mostly solved, which is why stage 4 is starting now. Second, honest data. A contract that pays on a weather reading is only as honest as the weather feed. This is called the oracle problem, and it is not solved, only managed: multiple independent feeds, signed sensor data, penalties for lying. Managed is enough for hail insurance. It is not yet enough for everything. Third, and hardest: control. Stage 4 asks a company to let a contract release payment instead of a manager. That is not a technology question. It is an auditor question, an insurer question, a board question. Every automated payment removes a small piece of someone’s control, and control systems defend themselves.

Stage 5’s obstacles are law, money, liability, and the world itself. When a settlement chain crosses five industries and three borders, whose law applies? The EU’s MiCA rules regulate tokens. No law anywhere yet covers an autonomous cascade, and when one misfires, nobody knows who is liable: the designer, the operator, or the data provider. Courts have no precedent. Then the money leg. Machines cannot open bank accounts, and a cascade cannot wait three days for a wire, so stage 5 needs money that moves at contract speed. Stablecoin legislation has now passed in the US and MiCA is in force in Europe, which is the right direction, but there is a decade of plumbing between “legal” and “your pension fund’s bank settles in it.” Then incentives. Every intermediary a cascade removes is a company with revenue and lobbyists: brokers, clearing houses, claims adjusters. They will not leave quietly, and some of the friction in today’s system exists because someone profits from it. And finally the world gets a vote. A world splitting into trade blocs splits its settlement rails too. Sanctions make programmable money attractive to some governments and threatening to others. If globalization keeps retreating, stage 5 arrives regionally rather than globally: a European metabolism, an Asian one, an American one, connected by narrow bridges.

The tailwinds. Working against all of that, two curves point up. The first is AI. Software agents are starting to transact, and an agent cannot wait three days for a wire or sign a paper mandate. Machine-speed commerce demands machine-speed settlement, so every step of AI adoption pulls these rails forward whether traditional finance is ready or not. This is why we run AI agents through the same engine with our sister product, Stategram. The second is the direction of the crypto rails themselves. Pieter Levels, a founder with a decent record of catching trends early, keeps a chart of long-run trend trajectories at levels.io/the-everything-chart. He calls it, in his own words, a subjective brain dump, and it proves nothing. But the two lines that must rise for stage 5 to exist, crypto and AI, are the two lines he draws climbing through the next decade. I would not bet a company on someone else’s chart. It is still nice when the chart agrees.

Ten years is not pessimism. It is a to-do list, and every item on it is being worked on right now.

What you can do now: make being wrong cheap

You do not wait for stage 5 to start. The deals that are signable today are stage 3, and every stage 3 deal builds a piece of the wiring. The problem is that every one of those deals is the first of its kind, and first-of-kind is expensive to attempt.

A template tokenization platform serves the eighth deal in a category, not the first. The schema is fixed. Your deal bends to fit, or it does not fit at all. Custom development handles novelty at a price: six to twelve months, a five-to-six-figure security audit, and a clock that restarts every time legal changes a rule. Which legal will, several times, because nobody’s first draft of a novel structure survives contact with counsel and counterparties. Run that math and a stage 3 experiment costs like a capital project and might return nothing. Most companies rationally do not try.

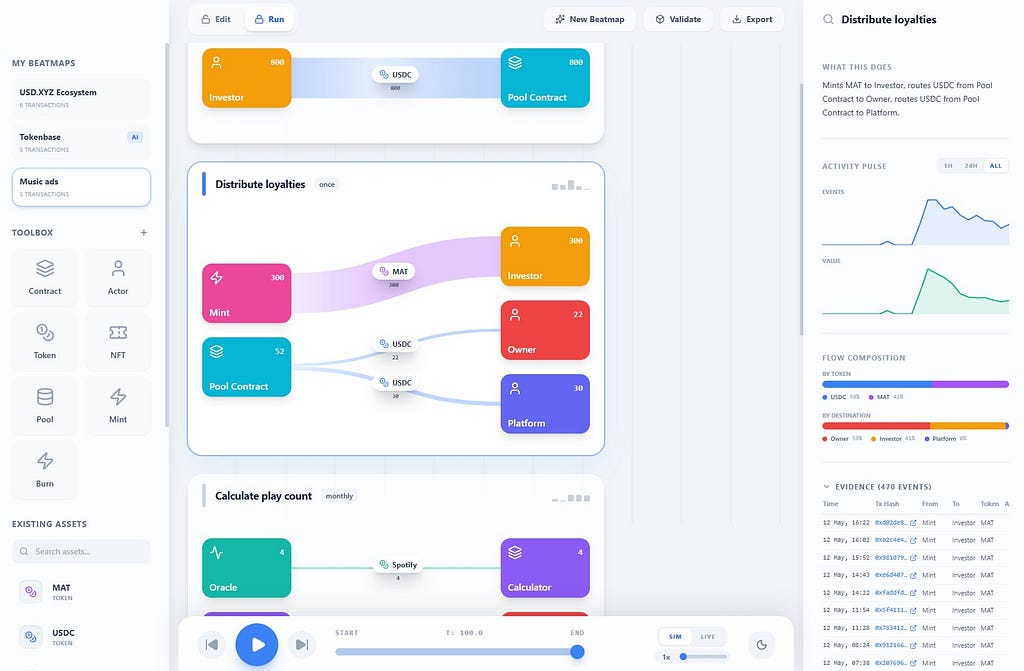

Three things collapse that cost. First, the structure has to be legible: not Solidity, which none of your stakeholders can read, but a lifecycle diagram all of them can. States, roles, payment rules, drawn as a workflow. The expensive part of a novel deal is alignment between legal, compliance, the board and counterparties, and when everyone reads the same diagram, iteration happens in the meeting instead of in a development sprint. Second, the contract has to be composed, not written. If the generated contract is assembled from independently audited building blocks, reviewers check a small, readable composition instead of novel code. Hours or days, not weeks. Third, change has to cost minutes. Legal adds a 30-day redemption notice: redraw the state, recompile, done. The prototype you test with real counterparties becomes version one of the production system, not a throwaway.

This is what we spent four years turning Toolblox into. More than 6,000 asset lifecycles have been designed on it since 2022, across stablecoins, funds, prediction markets and DePIN networks.

One deal at a time

Stages 3, 4 and 5 will not arrive as a wave. They arrive one first-of-kind deal at a time, built by teams who could afford to find out whether their structure works.

If you are holding one of those structures, something no platform template fits, the cheap way to find out is to map it. That is what our fixed-fee two-week audit is for: two weeks, your deal logic, jurisdiction, custody and edge cases, and a straight answer. Worst case, you learn exactly where your structure breaks. Best case, you are live at stage 3 while everyone else is still optimizing stage 2.

[Request a tokenization audit → https://www.toolblox.net/#audit]

Silver Sepp is the founder of Toolblox, a tokenization studio in Tallinn, Estonia.

Originally published on Medium.